Key Takeaways:

- Money laundering involves three stages: introducing illicit money (placement), obscuring its origins (layering), and making it appear legitimate (integration).

- Common laundering methods include using small transactions to avoid detection, employing mules to move money, exploiting casinos, using cryptocurrencies for anonymous transactions, blending illicit funds in cash-intensive businesses, buying valuable commodities, and operating shell companies.

- In traditional banking, anti-money laundering measures involve Know Your Customer (KYC) and Customer Due Diligence (CDD) processes with document verification and risk assessment. Sophisticated software is used for transaction monitoring, but compliance can be expensive and complex.

- In cryptocurrency, KYC is conducted digitally through online verification and facial recognition. Blockchain technology offers transparency for tracking transactions but raises privacy concerns. Regulatory frameworks are still developing and less established than traditional finance.

Money laundering has been a prominent problem in both the crypto world and traditional banking. However, in today’s age of digital currencies and decentralized finance, the old ways of money laundering have found new avenues. Traditional banking and cryptocurrency face distinctive challenges and employ various strategies to combat money laundering. This blog explores the complexities of Anti-Money Laundering (AML) in different contexts, highlighting their differences, measures, and socio-economic impacts.

To fully understand Anti-Money Laundering in cryptocurrency and traditional banking, it’s crucial to first comprehend how money laundering operates. This process, often intricate and multi-layered, consists of several stages designed to disguise the illicit origins of money and integrate it into a legitimate financial system. Here’s an in-depth study of how money laundering works and how AML strategies are deployed to counteract it.

Understanding Money laundering

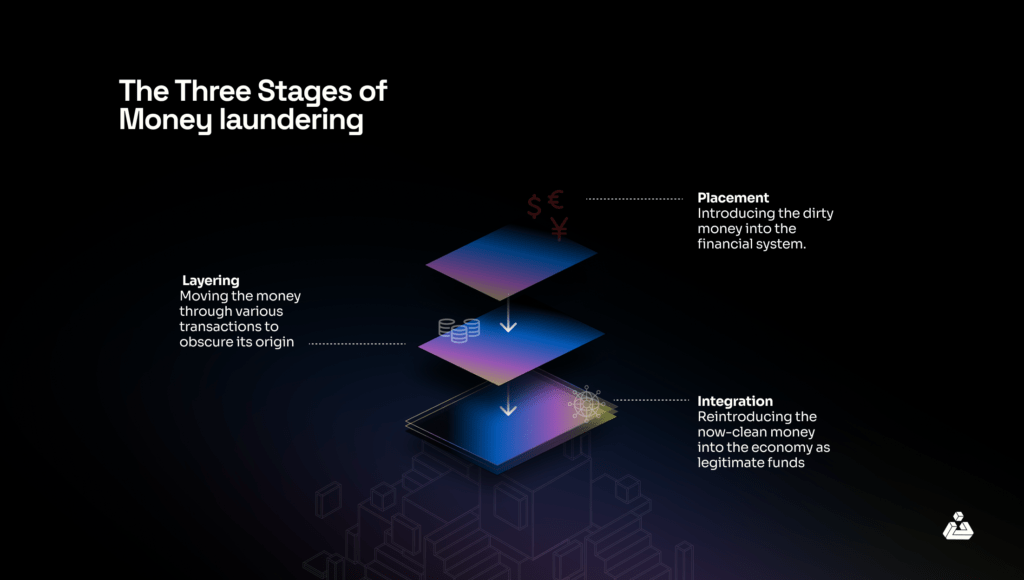

Money laundering is the process of concealing the origins of illegally obtained money, typically by means of involving foreign bank transfers, complex transactions, or legitimate businesses. It aims to make the illicit funds appear to be legitimate. Laundered money could be used to finance terrorism, develop illegal weapons, evade taxes, corruption, etc.The stages involved in money laundering are depicted below:

The Three Stages of Money laundering

eg: A drug dealer deposits $9,000 in cash (dirty cash) into a bank account over multiple days to avoid triggering mandatory reporting requirements. (Placement). The dealer then transfers the deposited money into several offshore accounts in countries with strict bank secrecy laws. The funds are used to purchase luxury cars. (Layering) . The dealer sells the luxury cars, using the proceeds to invest in a legitimate restaurant business, making the money appear as clean, legitimate revenue. (Integration).

Common Money Laundering Methods:

Smurfs

It is a term used to describe a money launderer who wants to avoid government scrutiny. They do this by using placement, layering and integration steps to conceal the money. Large amounts of money are deposited in different banks using smaller transactions. By doing this, they are able to dodge financial regulators and make it look like the money they deposit is legitimately sourced.

Mules

Just like drug mules, money mules carry illegal money for launderers. They may be aware of the scheme or recruited unknowingly with promises of high-paying jobs. Money mules open bank accounts and deposit illicit funds, which are then moved around using wire transfers and currency exchanges to avoid detection.

Gambling/Casinos

This involves buying casino chips with dirty money, minimal gambling, and then cashing out as ‘winnings’. For eg: Laundering $100,000 through a casino and cashing out $90,000 in clean funds.

Cryptocurrency

Using digital currencies for their decentralized and pseudonymous properties. For eg: Buying Bitcoin with illegal cash, transferring it through various wallets, and converting it back to fiat in a lenient jurisdiction.

Cash-Intensive Business

This refers to blending illicit funds with legitimate business revenue. For eg: If a restaurant makes $1000 a day, the owner might report $1500 by adding $500 of illegal money. This extra money gets mixed with the restaurant’s legitimate earnings, making it look like all the money is clean.

Mobile commodities (Gems, Gold)

Purchasing valuable items with illicit funds and selling them in different places to get clean money. For eg: Buying diamonds and selling them abroad to deposit the proceeds as clean money.

Shells

Business without operations, significant assets, or employees. They tend to conceal illicit activities, avoid taxes, and facilitate money transfers.

Socio-Economic Impact of Money Laundering

Money laundering has profound socio-economic impacts, particularly on developing countries. Socially, it undermines public trust and increases the cost of governance. Governments facing money laundering often need to allocate more resources to law enforcement and public welfare, reducing funding for other critical services and diminishing overall public welfare. This dynamic fosters a cycle of corruption and inequality, as illicit funds divert economic power from legitimate citizens and institutions to criminals, which can destabilize political systems and reduce overall societal trust in institutions.

Economically, money laundering destabilizes financial institutions and markets. It distorts investment flows, discourages foreign investment, and undermines economic stability. The influx of laundered money into various sectors can inflate asset prices, encourage inefficient resource allocation, and increase the risk of financial instability. Developing countries, with their fragile financial systems, are particularly vulnerable, facing weakened financial institutions, increased corruption, and reduced tax revenues. This hampers their economic growth and development, further entrenching their reliance on unstable economic practices.

Decoding Anti-Money Laundering

Anti-money laundering (AML) refers to a set of laws, regulations, and procedures designed to prevent criminals from disguising illegally obtained funds such as legitimate income. The primary goal is to detect and deter activities related to money laundering, which involves concealing the origin of money derived from criminal activities such as tax evasion, drug trafficking, human trafficking, and corruption.

While the general concept of AML is the same in traditional banking and cryptocurrency, the methods of money laundering and AML countermeasures employed differ, given the landscape they operate in. Both sectors rely on essential components, Know Your Customer (KYC) and Customer Due Diligence (CDD) , but implementation varies due to the unique traits of blockchain; decentralized, public, and immutable. Let’s explore how AML in Traditional banking differs from AML in crypto, and how blockchain can bridge the gap in mitigating financial crimes.

AML in Traditional Banking

The banking sector is identified as a main channel for laundering illicit funds, given their dual access to banking mechanisms and legal authority to make decisions. Money launderers and terrorism financiers find convenient access to these institutions, which facilitate a wide array of financial transactions, both domestic and international. The increasingly stringent Anti-Money Laundering (AML) and data protection regulations have compelled many financial entities to implement extensive and costly compliance procedures.

QUICK FACT

“The global financial system faces significant costs in combating money laundering, with compliance expenditures reaching $213 billion in 2020.” [1]

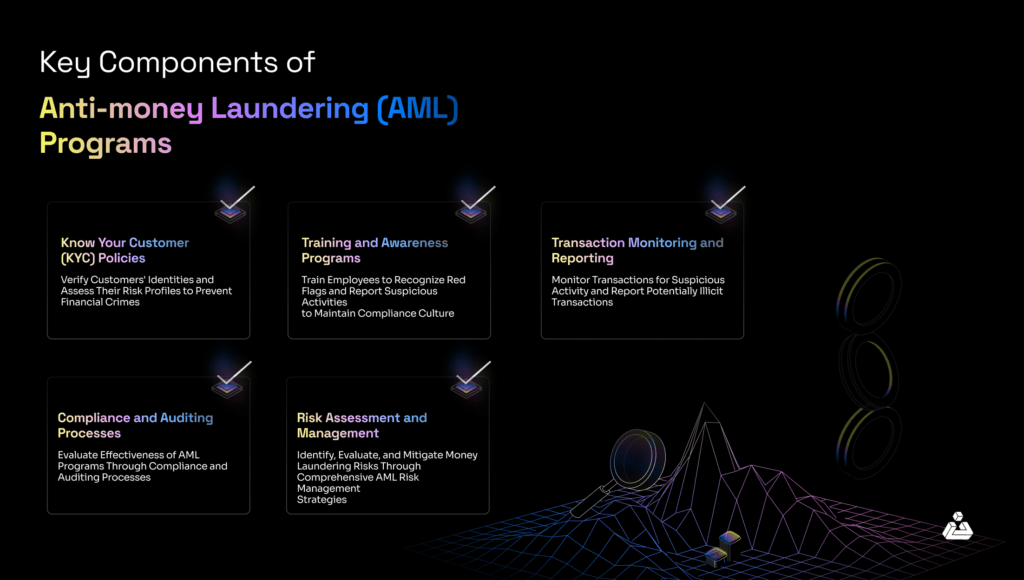

Components of AML

Traditionally banks, as well as other financial institutions use an architect method for identification [1] , referring to a structured and systematic approach to verifying customer identities, an essential tool to combat money laundering (ML) and terrorist financing (TF). This commonly includes traditional paper document verification i.e. physical documents like passports, ID cards, driver’s licenses, utility bills, and digital documents such as scanned copies of ID cards. Moreover, biometric verification includes digitized fingerprint scans to match a person’s identity against government databases, facial recognition, voice recognition, or iris scans.

KYC (Know your Customer) and CDD (Customer Due Diligence) are fundamental components of AML compliance. They are similar in that both aim to verify customer identities and prevent financial crimes. While KYC is a process used by financial institutions to verify the identity of their clients and to know who their customers are, CDD is a simple check to assess the risk posed by customers based on their activities and background. In the banking sector, it is a normal practice for customers to provide identity documents like a passport, ID, and proof of address. The bank verifies these documents, cross-checks them with existing databases, and assigns a risk level based on the customer’s profile according to the CDD levels defined.

Risk assessment and management involve evaluating and managing risks. If a customer is deemed low-risk, an SDD (Simplified Due Diligence) approach is taken and only basic information is collected. On the other hand, if a customer is deemed high risk due to connections to high-risk jurisdictions or high-value transactions the bank conducts EDD (Enhanced Due Diligence), which might include detailed background checks and continuous monitoring of transactions.

Transaction monitoring and reporting consists of continuous review of financial transactions to detect and report suspicious activities, The purpose of this process is to identify patterns that could indicate money laundering or terrorist financing. For eg: banks use sophisticated software to monitor transactions and flag unusual activities for further investigation. Compliance and auditing ensure that all internal processes adhere to regulatory standards, with regular audits conducted to verify compliance and maintain the integrity of institutions AML’s efforts.

Training and awareness programs are crucial, as they train employees to recognize red flags and maintain compliance. Regular training sessions ensure that staff are up-to-date with the latest AML regulations and practices, enabling a culture of vigilance and accountability within the institution. These key components serve as a core foundation of AML.

Let’s explore a brief case study to understand how these are being applied in the real world.

Case study: Standard Chartered Bank Under Sanctions Compliance Challenges

Background

The US Department of Justice (DOJ) announced that Standard Chartered Bank (SCB) agreed to a settlement involving the forfeiture of $240 million, an extended Deferred Prosecution Agreement (DPA) of two years, and a fine of $849 million. This action came after SCB was found to have facilitated thousands of financial transactions for sanctioned entities, including Iran, in apparent violation of the International Emergency Economic Powers Act (IEEPA)

Key Takeaways:

- SCB strengthened its internal controls and developed more robust AML policies to ensure a higher compliance standard.

- The bank introduced more stringent customer due diligence processes to better screen and onboard foreign clients.

- SCB adopted advanced technology solutions to streamline AML screening processes and improve the efficiency of compliance checks.

- SCB set a proactive stance towards compliance, which included regular updates to compliance protocols in response to evolving regulatory landscapes.

- Employees were educated on the importance of adhering to compliance protocols through comprehensive training programs.

In the traditional banking sector, complying with AML regulations poses substantial challenges. As existing regulatory frameworks or technology can be bypassed by the violators, with rapid evolution of digital systems and global financial transactions, prevention and detection of sophisticated money laundering schemes is becoming complicated. Moreover, the high costs associated with implementing and maintaining robust AML programs strain financial resources, particularly for smaller institutions. These limitations call for a robust solution, like blockchain technology which is capable of bridging these gaps.

AML in Crypto

Blockchain offers a transformative solution to traditional Know Your Customer (KYC) processes which face significant inefficiencies, as viewed earlier. These processes are often time-consuming, costly, and prone to human error, resulting in a fragmented approach to customer verification. Repeatedly collecting and verifying the same customer info leads to redundancy and increased operational costs. Criminals can easily exploit the lacking in KYC process. Some of the main issues in the KYC process are as follows[1]:

- Elevated costs due to redundancy

- An excruciatingly long process that leads to poor customer experience

- New KYC registration for every institution which leads to a bad experience

- Hefty fines due to compliance with ambiguous processes

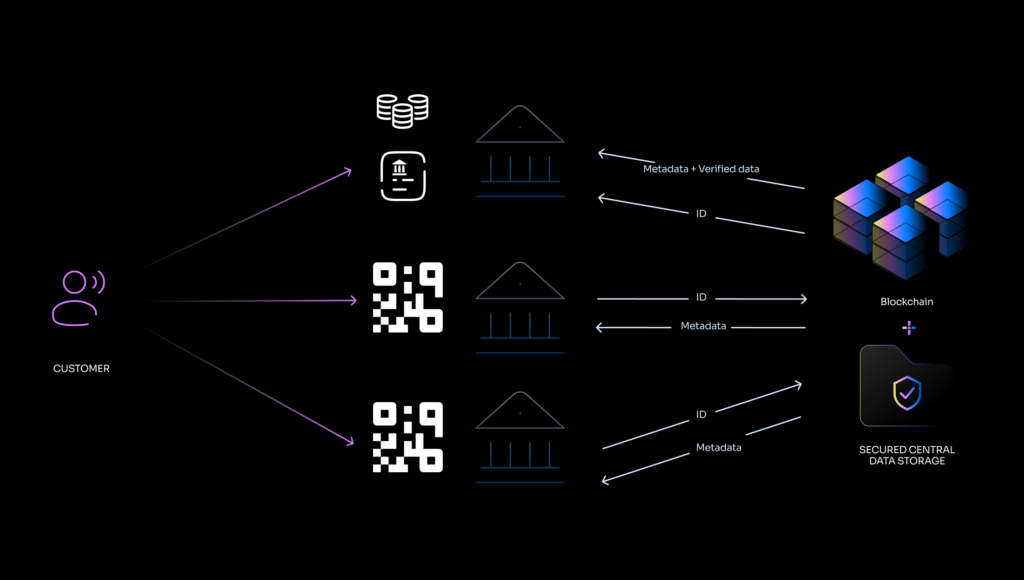

The diagrams below depict how cutting-edge technology can streamline the KYC process.

Privacy Protection & Reduce Fraud Faster.

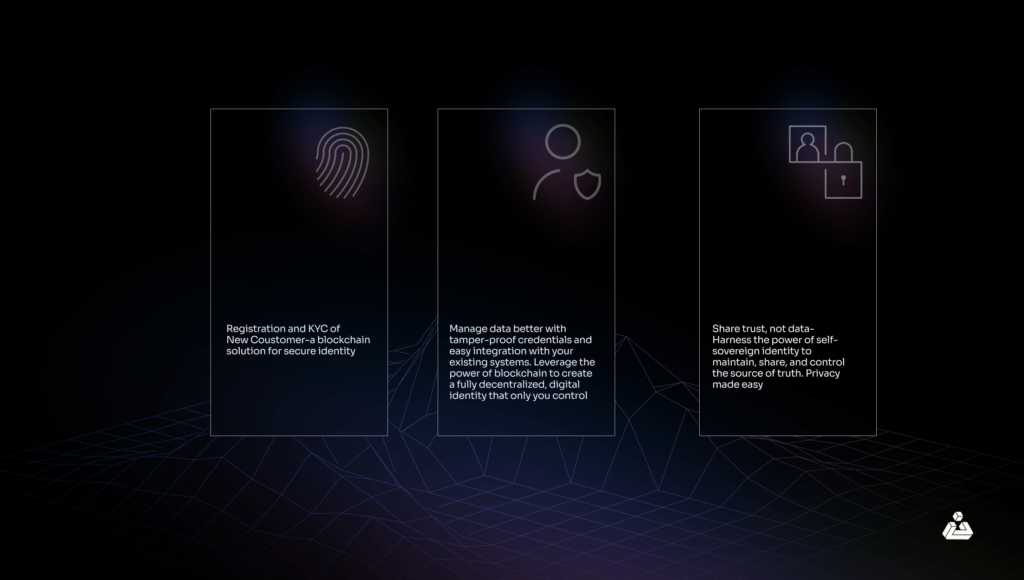

The proposed KYC system

By leveraging a distributed ledger system, blockchain enables a secure, immutable, and transparent record of customer information that can be accessed by authorized parties in real-time. This technology allows for the creation of a single, verified digital entity, eliminating the need for redundant data across multiple financial institutions. Blockchain’s consensus mechanism ensures that all transactions are verified and time-stamped, providing a reliable audit trail that enhances transparency and trust. Additionally, blockchain’s inherent security features protect against data tampering and unauthorized access, reducing the risk of fraud.

Implementing a blockchain-based KYC framework involves several critical steps to ensure effectiveness and compliance. First, financial institutions need to adopt a blockchain platform, such as Hyperledger Fabric, which facilitates secure and efficient identity management and credential verification. The process starts with secure credential registration and the administration of KYC documents on the blockchain, followed by a lightweight verification procedure between customers, financial institutions, and the blockchain platform. Additionally, the system must incorporate mechanisms to counter remote and spoofing attacks to protect the integrity of the KYC process .

Components of AML in crypto

The components of AML in crypto slightly differ from conventional banking setup. Let’s see how they are different and add to effectiveness but just before that, we will understand the concept of crypto assets and crypto asset providers.

Crypto assets, also known as virtual assets, are digital representations of value that can be transferred, stored, or traded electronically. The unique nature of these assets, characterized by decentralization and anonymity, poses significant challenges for implementing Anti-Money Laundering (AML) measures. Crypto asset providers, recently brought under AML obligations, must now implement Know Your Customer (KYC) and Customer Due Diligence (CDD) processes similar to traditional financial institutions.

The Financial Action Task Force (FATF) issued updated guidance in October 2021, detailing a risk-based approach to virtual assets and virtual asset service providers. This guidance helps countries and entities identify which crypto-related activities fall under AML regulations. It clarifies the definitions of “virtual asset” and “virtual asset service provider,” showing the differences between the activities of crypto asset providers and traditional financial institutions. These distinctions are crucial for applying FATF recommendations and considering the money laundering (ML) and terrorist financing (TF) risks associated with crypto activities.

Coming to the components of AML, crypto providers serve customers online and use special verification tools to mitigate the risk of unmatched verification documents. The onboarding procedure is simple as compared to visiting a bank to open an account because crypto providers offer different account levels depending on the degree of verification. This method often eliminates the need for paperwork, digitizing the verification process using advanced tools and facial recognition as part of their KYC (Know Your Customer) and CDD (Customer Due Diligence) procedures. In KYC, Zero-Knowledge Proof (ZKP) allows a user to prove their identity to a verifier without disclosing actual personal data. The user provides cryptographic proof that they possess certain attributes (e.g., age, nationality) verified by a trusted third party, which the verifier can confirm.

While blockchain’s decentralized and immutable nature might complicate transaction monitoring, blockchain analytical tools allow detailed tracing of funds, assisting in identifying criminal activities when converting crypto to fiat currency. Additionally, crypto providers implement risk assessment and management strategies to evaluate and manage potential threats. Training and awareness programs ensure that employees are well-equipped to recognize and handle suspicious activities, maintaining robust reporting protocols for compliance with AML regulations.

Bloom, a credit score platform, leverages blockchain technology to enable users to create blockchain-based profiles through its mobile app. In addition to this, Bloom offers an identity monitoring program that constantly scans both the open and dark web for any signs of client data breaches. Their latest compliance solution, OnRamp, features ID verification and sanction screening, as well as Politically Exposed Person (PEP) screening. OnRamp also integrates with Plaid, allowing users to link and verify their bank account information.

Quadrata is another company that provides Know Your Customer (KYC) solutions on the blockchain. Recently, Quadrata secured $7.5 million in seed funding to enhance the functionality of its Ethereum-based Quadrata Passport. This Passport, a non-transferable NFT, stores information necessary for compliance with KYC and anti-money laundering (AML) requirements.

Similar innovations have been piloted by HSBC, Deutsche Bank, and Mitsubishi UFJ Financial Group, which have experimented with using blockchain technology to exchange KYC information. This initiative ensures the secure digital preservation of consumer data, reducing the redundant collection of the same data by competing financial institutions.[1]

Key Takeaways:

- Continuous surveillance for data breaches through blockchain-based identity monitoring

- Integration of ID verification, sanction, and PEP screening in compliance solutions like Bloom’s OnRamp.

- As exemplified by Bloom’s integration with Plaid for bank account verification, bridging banking systems with blockchain technology.

- Secure storage of compliance data using NFTs, as seen with Quadrata’s Ethereum-based passport.

- Reduction of redundant data collection, as showcased by HSBC, Deutsche Bank, and Mitsubishi UFJ Financial Group’s pilot project.

Blockchain technology offers significant advantages for KYC use cases, such as enhancing security, reducing redundancy, and improving efficiency through immutable and transparent records. However, it is not entirely effective in data monitoring and cannot completely eliminate the risks of fraud or terrorist financing, as criminals have found ways to bypass these systems. We will see later in the article, that combining blockchain with AI tools and other advanced technologies can further bolster AML compliance measures.

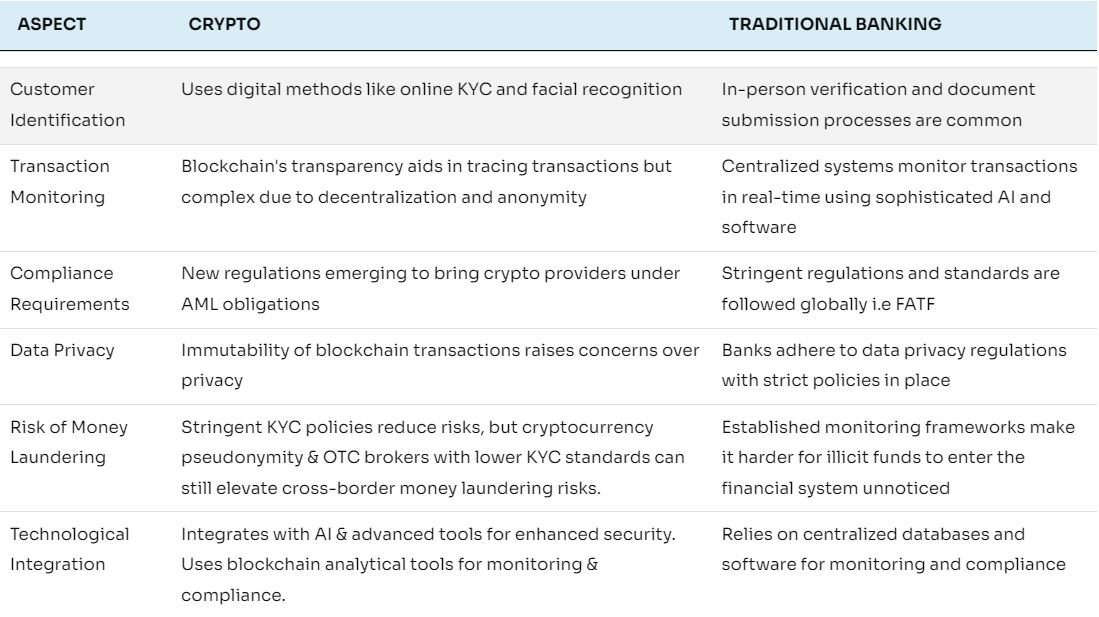

Quick Summary (AML in Crypto vs Traditional Banking)

Conclusion

Money laundering remains a significant challenge due to individuals disguising illegal funds as legitimate. Traditional AML approaches lack the necessary transparency and efficiency, prompting financial institutions and authorities to explore innovative strategies. Blockchain technology emerges as a promising solution, offering a secure, efficient, and transparent platform for user identification and verification, enhancing AML compliance, and addressing identity management issues. However, blockchain’s potential is fully realized only by addressing its inherent risks and challenges, especially in banking and financial services.

While blockchain streamlines the KYC process, it does not entirely eliminate the challenges of transaction monitoring and fraud risks. To mitigate the global impact of money laundering, governments and financial institutions must adopt advanced technological solutions like blockchain alongside AI/ML tools for monitoring and AML regulatory compliance. These technologies can enhance regulatory compliance and user experience, providing a comprehensive approach to safeguard financial institutions from substantial financial losses.