The cryptocurrency landscape is characterized by a dynamic array of token launch models, each designed to achieve a delicate balance between liquidity, fair distribution, and efficient price discovery. As the industry matures, projects are increasingly discerning in their selection of launch mechanisms to align with their specific goals and target audience, reflecting the adage that there is no “one size fits all” solution. This article explores the diverse spectrum of token launch models, from traditional fixed-price offerings to innovative approaches like Liquidity Bootstrapping Pools (LBPs).

Types Of Token Launches

With a foundational understanding of the overarching objectives, we will now delve into the specific mechanisms employed in various token launching models. Each approach presents distinct advantages and challenges, catering to different project goals and investor preferences.

Fixed Price

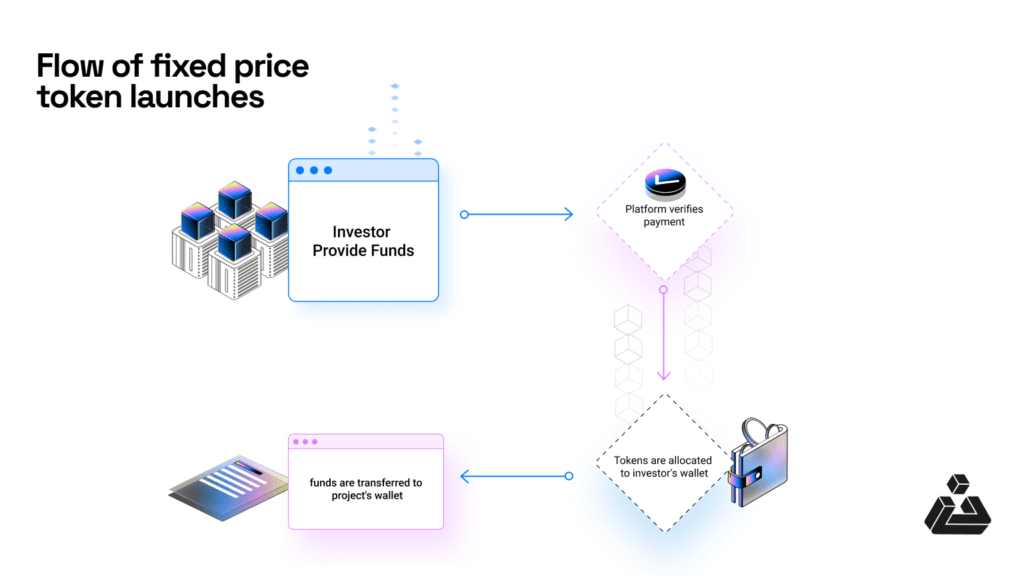

In the traditional cryptocurrency market, the most prevalent type of token sales is the fixed price token sale, encompassing Initial DEX Offerings (IDOs), Initial Coin Offerings (ICOs), and Initial Exchange Offerings (IEOs). In these models, price discovery is predetermined by the project itself, typically anchored to a specific fundraising goal. The distribution of tokens is structured accordingly to meet this target.

In a fixed price token launch, the token’s value is tied to a reference asset, such as a fiat currency (e.g., USD) or another cryptocurrency (e.g., ETH). The token’s price is set at the time of launch and remains fixed, regardless of market fluctuations.

For example, let’s consider a token launch with a fixed price of 1 USD per token. The liquidity pool (LP) is created with a specific ratio of reference asset (USD) to tokens, ensuring that the token’s value remains pegged to the reference asset.

When a user participates in the token launch, they receive tokens in exchange for a corresponding amount of the reference asset, based on the predetermined ratio. For instance, if the LP is set at 100 USD = 100 tokens, a user contributing 10 USD would receive 10 tokens.

The core calculation in a fixed-price token launch revolves around determining the token allocation based on the funds raised.

- Token Price: The set price at which each token is sold.

- Total Supply: The overall number of tokens available for sale.

- Hard Cap: The maximum amount of funds the project aims to raise.

- Token Allocation: The number of tokens received by an investor based on their investment amount.

This process was relatively simpler however keep in mind that when these launches happened we3 was relatively new.

The flow is quite simplified but based it this we can easily identify that this type of launch has a few key participants who are

- Project Team: The core group responsible for developing the project and conducting the token sale.

- Investors: Individuals or entities purchasing tokens in exchange for funds.

- Launchpad or Platform: The intermediary facilitating the token sale (e.g., Binance Launchpad, KuCoin Spotlight).

- Token Holders: Participants who successfully acquire tokens during the launch.

- Market Makers: Entities providing liquidity to the token after launch.

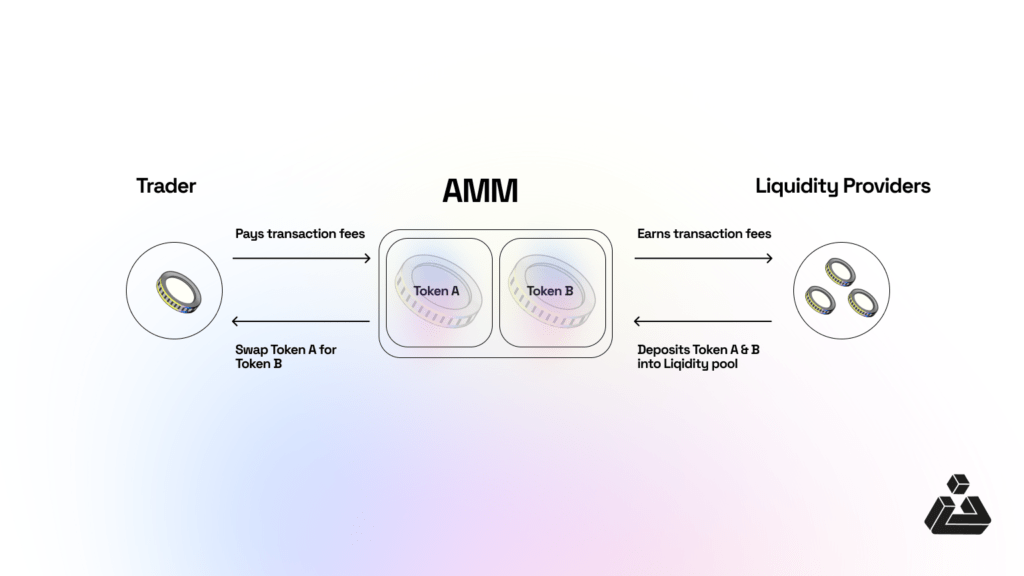

Uniswap V2 Style AMM Markets

In Automated Market Maker (AMM) systems, the pricing mechanism fundamentally differs from traditional Initial Coin Offerings (ICOs) or Initial Exchange Offerings (IEOs). Here, the token price is dynamically determined by the ratio of assets within the liquidity pool, adhering to a formula.

x.y = k.

Where x and y represent the reserved balance of two distinct tokens.

This formula ensures that the product of the two token amounts always remains constant. As a result, when traders swap one token for another, the ratio of tokens in the pool adjusts, affecting the price.

Typically, in an Initial DEX Offering (IDO) utilizing an AMM, the project initiates the process by contributing liquidity for both the project asset and a reserve asset, usually in a 50:50 ratio. This initial step establishes the starting price of the token. Once the liquidity pool is activated for trading, market participants can swap the reserve asset for the project token and vice versa. These trading activities continually adjust the token’s price, allowing the market to discover its fair value organically.

For example, a new token is introduced to a liquidity pool with an existing token, say ETH. The initial price is set by the ratio of tokens in the pool. For instance, if a project contributes 100,000 new tokens and 100 ETH to a pool, the initial price of the new token is 1 ETH. As trading begins, the price fluctuates based on buying and selling pressure, adjusting the token ratio within the pool. If there’s strong buying pressure, the price increases, and the token ratio shifts towards more ETH and fewer new tokens. Conversely, if selling pressure dominates, the price decreases, and the token ratio shifts towards more new tokens and fewer ETH. Let’s say selling pressure drives the pool to 150 ETH and 50,000 new tokens; the price would drop to 0.33 ETH per new token.

It’s crucial to distinguish that such styled IDOs are primarily geared toward ensuring deep liquidity on a Decentralized Exchange (DEX). In contrast, fixed-price IDOs often involve collaboration with a third-party decentralized launchpad to facilitate the sale. After raising capital through these means, the project then establishes a liquidity pool on a DEX. This approach allows the secondary market to commence, further influencing the token’s market value and liquidity post-launch.

The Flow of token in a Uniswap v2 style AMM Market clearly shows us the entities involved in this which are

- Liquidity Providers: Contribute funds to create liquidity pools.

- Traders: Facilitate token swaps by interacting with the liquidity pools.

- Protocol: The underlying smart contract system that manages the liquidity pools and swaps.

Dutch Auctions

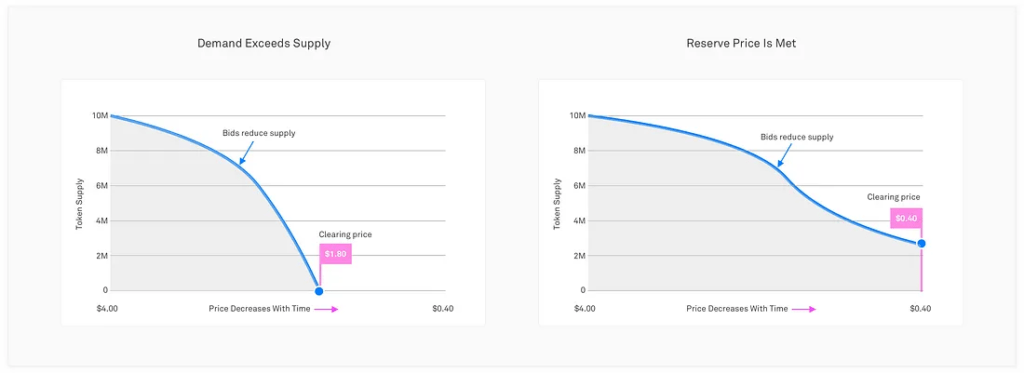

In a Dutch auction, the token pricing follows a pre-defined trajectory, starting from an initial high price and gradually descending towards a predetermined lower reserve price. Participants in this model have the flexibility to purchase tokens at any point during this price decline, based on their valuation assessment. The auction concludes when the entire token supply is sold or the reserve price is met, with the final price being set at the point where the last token is purchased.

Source:https://medium.com/coinlist/a-primer-on-dutch-auctions-525036d24d10

The successful bidders pay the price on which the auction ends.

The Algorand Foundation used a Dutch Auction model for their token distribution in 2019. The starting price of the token was $10 per token. 25% of the total tokens were allocated to a “community pool” for future development and grants, while the remaining 75% were sold to participants through the Dutch Auction. In the auction, the price of the token decreased as bids were submitted, ultimately settling at around $2.40 per token.

In the case of such auctions, the key partners comprise of

- Project Team: Sets the auction parameters and manages the token distribution.

- Investors: Participants who purchase tokens during the auction.

- Auction Platform: The platform hosts the auction and manages the token distribution.

This method not only fosters a broader distribution of tokens but also effectively mitigates the risk of market manipulation by bots or large-scale investors. Notably, the Liquidity Bootstrapping Pool (LBP) is an innovative adaptation of the Dutch auction, drawing inspiration from its foundational principles and mechanics.

Lockdrop + Liquidity Bootstrap Auction

The Lockdrop + Liquidity Bootstrap Auction (LBA) model presents an innovative approach for fair market price discovery and broad token distribution introduced by Delphi Digital. This method unfolds in two distinct phases: the lockdrop and the LBA.

Phase 1: Lockdrop

- A time-window where users can pre-commit to become users of a particular protocol.

- Participants receive a proportional share of tokens based on the length of commitment and size of tokens held. This phase emphasizes rewarding future contributions rather than past actions, ensuring a fair and forward-looking distribution of tokens.

- These tokens are locked until Phase 2 ends.

Phase 2: Liquidity Bootstrap Auction (LBA)

- The LBA phase serves as the price discovery stage.

- Protocol users are granted the previously locked tokens and allowed to sell them through an auction.

- Participants from the lockdrop can choose to become liquidity providers by depositing their rewarded tokens. Others, particularly those without lockdrop rewards, can contribute by supplying the other half of the liquidity pair, often a stablecoin.

- At the end of the LBA, both the project tokens and stablecoins are pooled in a 50/50 liquidity pool, the dynamics of which establish the final market price of the project token.

- The auction establishes a market price for the tokens, providing instant liquidity.

Mars protocol and Astroport used this mechanism to launch their tokens. In Astroport, deposits were allowed for 5 days. On day 6, users could withdraw 50% of their tokens, with just one transaction being allowed. On day 7, withdrawal limits linearly declined from 50% to 0 throughout the day. The need for this component stemmed from the fact that without it, whales can deposit considerably more than they plan on leaving in the pool to inflate the price well beyond what they’d want to pay to discourage other participants.

This dual-phase approach effectively addresses the trifecta of distribution, price discovery, and liquidity challenges in token launches, offering a comprehensive and balanced solution.

Liquidity Bootstrapping Pool (LBPs)

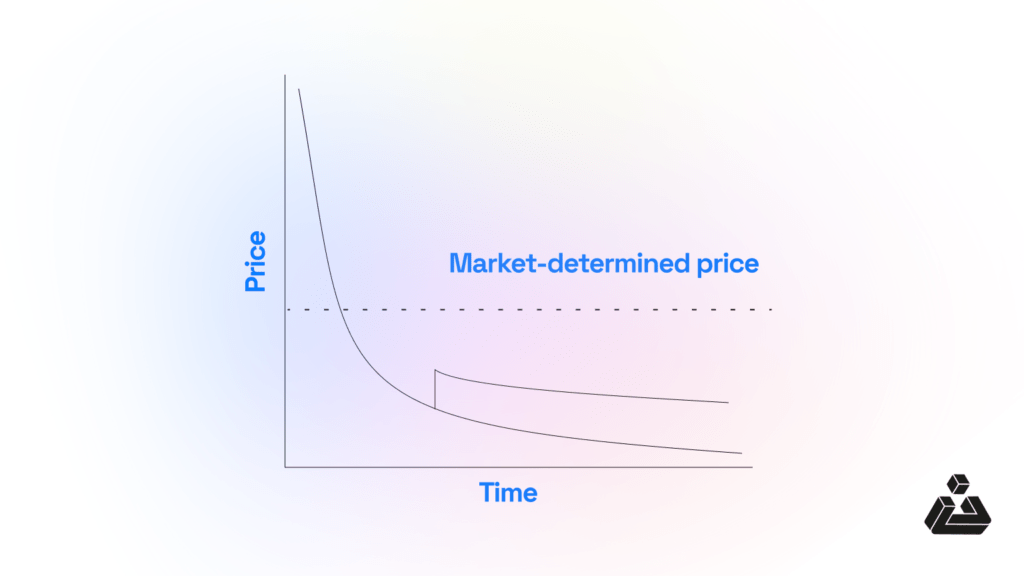

A Liquidity Bootstrapping Pool (LBP) is an innovative mechanism designed for token launches, offering a transparent and equitable distribution of tokens with market-driven price discovery. Central to its functionality is a declining price curve, which is systematically adjusted through pre-defined starting and ending weight parameters. This gradual reduction in price allows participants the flexibility to engage at their preferred price points. Initially set at a higher value, the starting price effectively discourages manipulation by bots and whales, thereby upholding the integrity of the sale process.

Now, let’s have a look at the key components of LBP

- Weight Ratios: The core of the LBP is the dynamic adjustment of weight ratios between the new token and the reserve asset. These weights determine the price of the token at any given point during the launch. For example, a higher weight for the new token implies a higher price.

- Price Curve: The LBP’s price curve is a visual representation of the token’s price trajectory over time. It is determined by the initial and final weight ratios, as well as the duration of the LBP.

- Reserve Assets: LBPs typically accept multiple reserve assets, such as stablecoins (e.g., DAI, USDC) and/or WETH, to facilitate token sales and provide liquidity.

- Initial Token Sale: The LBP starts with an initial token sale, where the project sells its tokens to investors.

- Weight Ratios: The LBP controller adjusts the weight ratios of the token sale, influencing the token’s price. The ratios can be customized to achieve a desired price curve.

- Reserve Assets: The LBP can accept multiple reserve assets, such as stablecoins (e.g., DAI, USDC) and/or WETH, to facilitate token sales.

- Price Discovery: The LBP’s price discovery mechanism ensures a fair market value by starting at a higher price and adjusting downward as the sale progresses.

A Basic Comparison to sum it up

| Feature | Fixed Price | AMM | Dutch Auction | Lockdrop + LBA | LBP |

| Price Discovery | Predetermined | Market-driven | Descending price | Market-driven with lockdrop | Market-driven with weight ratios |

| Liquidity | Dependent on market makers | High initial liquidity | Can be variable | High initial liquidity | High initial liquidity |

| Distribution | Based on investment amount | Based on liquidity provision | Based on bid price | Reward-based with LBA | Based on price and timing |

| Risks | Price manipulation, low liquidity | Impermanent loss | Price volatility, bot attacks | Potential for uneven distribution | Complex mechanism, potential for manipulation |

Conclusion

The token launch landscape is rich with diverse models, each catering to different needs and preferences. From fixed-price sales to dynamic AMM markets, Dutch auctions, and innovative LBPs, projects can choose the mechanism that best aligns with their goals. The evolution of these models reflects the industry’s growth and its ongoing quest for fair distribution, liquidity, and efficient price discovery. As the cryptocurrency space continues to evolve, we can expect further innovations in token launch mechanisms, each aiming to address emerging challenges and opportunities.

Your token deserves more than just a launch—it deserves a legacy. With our Token Launch Service, we’ll help you craft a launch strategy that isn’t just effective but unforgettable. Don’t just ride the wave—lead it. 🌊 Let’s build the future, together.

Explore More-Must Reads:

Token Utility: Use Cases & Trends

Utility Tokens vs. Security Tokens: Understanding the Difference